They promised to abolish the Belka tax. It was supposed to be simple, fair and motivating. Instead, we will get a new financial instrument in late 2026.

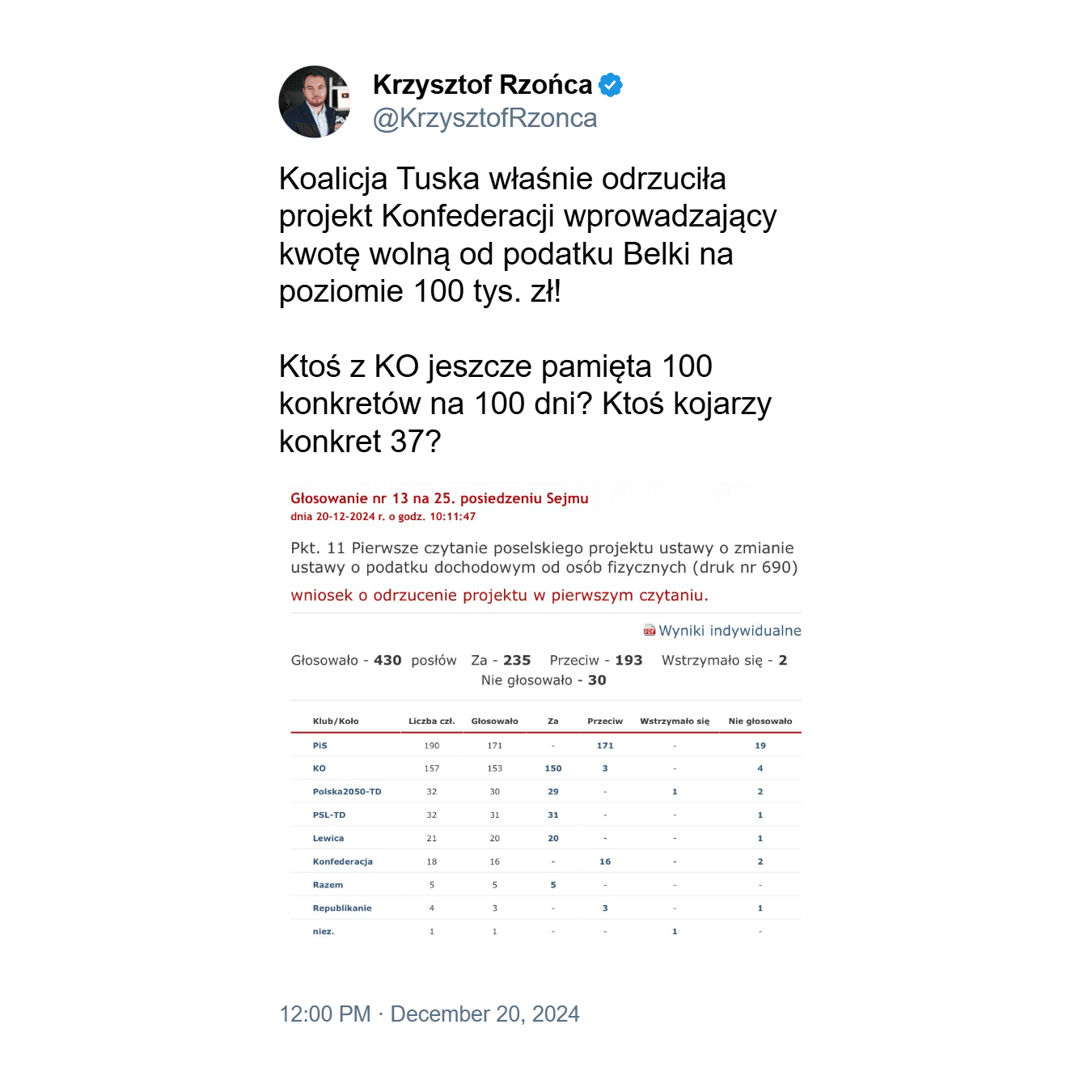

In the election campaign of 2023 Civil Coalition promised "100 specifics for 100 days". Under item 37, it is clearly stated: abolition of the Belka tax for savings and investments to PLN 100 thousand held for more than a year. Today we know that this promise will not be kept.

Instead, the Ministry of Finance and Economy (yes, the ministry changed its name in July) announced the creation of a new instrument: Personal Investment Account (OKI). An idea? Instead of eliminating tax for all, a new product is created. We will also have to wait for him until the second half of 2026.

A new financial instrument instead of a real reform

According to the announcement of Minister Andrzej Domański, OkI is to allow Poles to invest up to PLN 100,000 without the tax of Belka, and above this amount with a preferential tax rate of about 0.8-0.9% per year. The idea is inspired by the British ISA (Individual Savings Account), but in Poland the problem is not the lack of investment products, it is a mess, high taxation and complicated rules.

Some data on investing in Poland:

- Only 6% of Poles actively invest on the stock exchange (GPW, 2024).

- Among those aged 18-29, over 70% hold money only in savings accounts or cash (NBP, Financial Diagnosis 2024).

- Half of Poles cannot indicate what is different from IKE (BGK, 2023).

Nevertheless, instead of simplifying the tax system, we get another instrument that few people understand. And it would be much easier just to:

- introduce a capital duty-free amount,

- design a progressive tax scale that does not match a small investor with someone who makes millions on the stock market.

IKE, IKZE, PPE, which is how to discourage people from saving

It is not that Poles have no place to invest. We have IKE, IKZE and some are also offered Employee Pension Programmes. In theory, they are great products:

IKE: no tax on Belka after reaching retirement age and meeting conditions. Payment limit for 2025: PLN 23,472.

IKZE: in addition, payments can be deducted from income (limit: PLN 9 388.80 for non-business persons).

PPE: for lucky people working in larger companies who agreed to this benefit.

Unfortunately, most Poles do not know about it, either do not understand the principles of operation, or simply do not believe that the state will not change the rules of investment game again in a few years.

In addition, all of these products have one common denominator: they are rigidly linked to retirement age, which for young people means freezing funds for decades.

Investing is not a hobby. It's a necessity.

You don't need to be an economist to know that future ZUS pensions will be dramatically low. Today's 20-year-old boy, who doesn't invest consciously, probably doesn't have any protection for the future. Demography in Poland is merciless and the cost of living increases. How can a young man be motivated to put down money when the state collects 19% of Belka's tax on everyone, even the smallest profit?

All data and analyses indicate one thing: young Poles want to invest, but often do not know how, which creates the need to create simple and motivating paths for investing capital. The promise of "100 concretes" was a good step this way. Instead of implementing it, we have another instrument that forces you to change habits and has an uncertain future.